Why I Switched from BMO to Wealthsimple: A Personal Review

For most of my life, I did what most Canadians do by default:

I banked with one of the Big Three.

In my case, that was BMO.

It wasn’t terrible. It was just… expensive in ways I’d quietly accepted for years. Once I actually looked at the numbers and friction involved, I realized it didn’t make sense anymore.

The Chequing Account Fee That Finally Pushed Me Over

Here’s the moment it clicked for me.

With BMO, if I didn’t keep $4,000 sitting in my chequing account, I was charged $16 per month.

That’s $192 a year—just to access my own money.

To avoid the fee, I had two choices:

- Pay $16/month

- Or park $4,000 doing absolutely nothing

Neither felt reasonable.

I don’t want to lock thousands of dollars in a chequing account earning basically nothing just to avoid a fee. That money should be working for me—not being held hostage.

Once I framed it that way, the decision became obvious.

No Monthly Fees with Wealthsimple

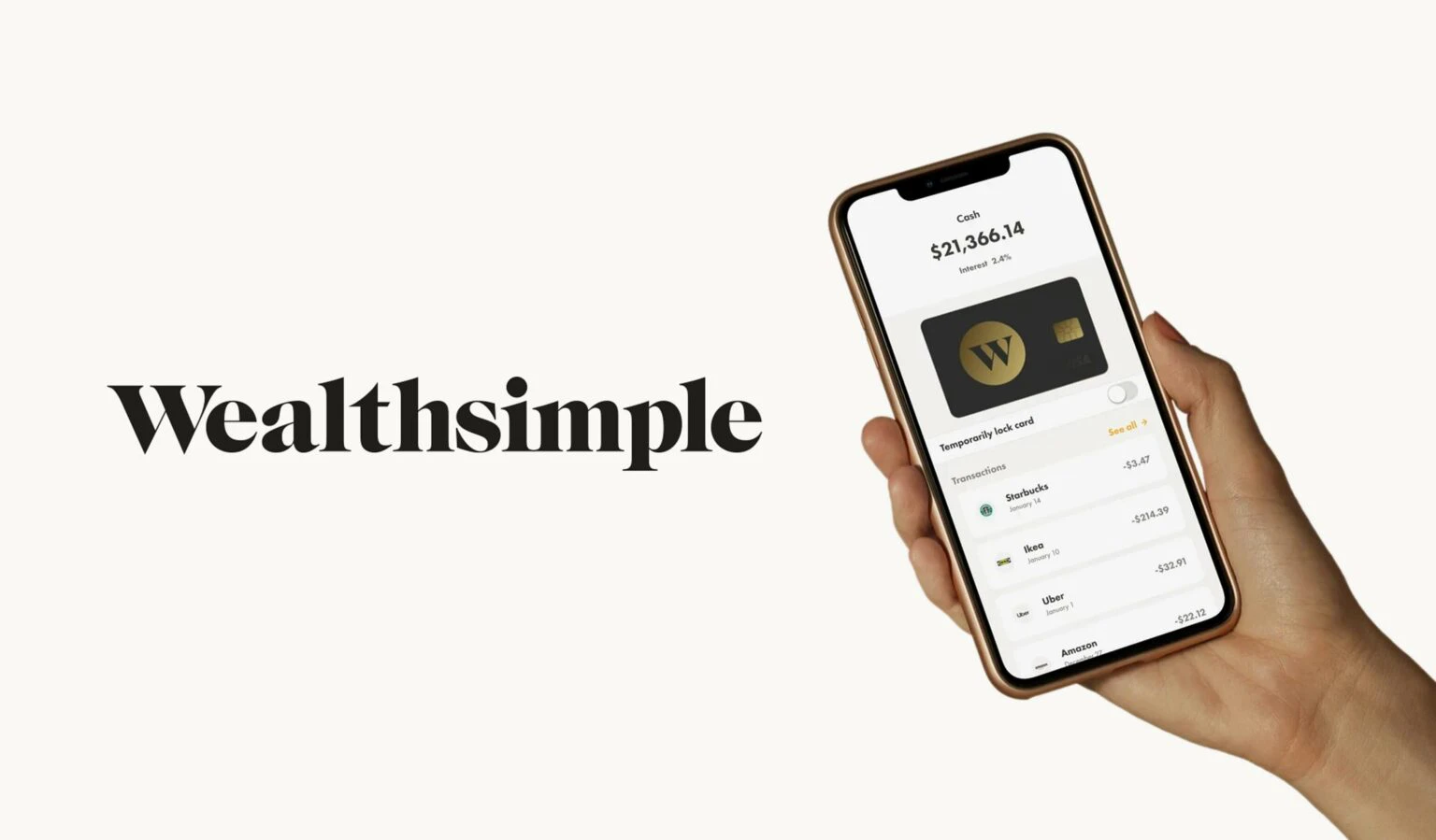

That’s when I started moving my money to Wealthsimple.

With Wealthsimple:

- No monthly account fees

- No minimum balance requirements

- No penalties for moving your money

Your cash just sits there—like it should.

Open an Account in Minutes (Not Days)

Opening accounts with traditional banks usually means:

- Branch visits

- Appointments

- Paperwork

- Waiting

With Wealthsimple, I opened my account in minutes from my phone.

Verification was quick, setup was painless, and I could start immediately.

It feels like it was built for people living in 2026—not 1996.

Everything in One App (RRSP, TFSA, Cash, Crypto)

This was a huge quality-of-life upgrade.

I now use Wealthsimple for:

- RRSP

- TFSA

- Cash

- Crypto

One app. One login. One clean overview of my money.

No more juggling:

- Multiple bank apps

- Different interfaces

- Different support teams

It’s simple, clean, and actually enjoyable to use.

Free Tax Filing (This One’s Underrated)

This part doesn’t get talked about enough.

Wealthsimple also lets me file my taxes for free.

No paying $30–$50 to a tax software.

No upsells.

No switching platforms.

My investments, tax slips, and filing all live in the same ecosystem, which makes tax season way less annoying than it needs to be.

For something that most Canadians deal with every year, having it bundled in for free is a big deal.

Crypto Without the Usual Headaches

Instead of dealing with separate platforms, transfers, and delays, I can buy crypto directly in the app.

Clear pricing. Clean interface. No sketchy steps.

For someone who wants exposure without turning it into a full-time hobby, it just works.

Live Chat Support That’s Fast and Human

This one surprised me.

The live chat support is:

- Fast

- Friendly

- Helpful

No endless hold music.

No bouncing between departments.

No “please visit a branch.”

Compared to traditional bank support, it feels like a completely different era.

Big Bank vs Wealthsimple (Real-Life Comparison)

Traditional Bank (BMO)

- $16/month chequing fee

- Fee waived only if $4,000+ stays idle

- Multiple apps and logins

- Slower, more rigid support

- Investing, savings, and crypto split across platforms

- Separate paid tax software

Wealthsimple

- No monthly account fees

- No minimum balance requirements

- RRSP, TFSA, Cash, and Crypto in one app

- Free tax filing

- Fast, friendly live chat

- Clean UI designed for everyday use

This isn’t about “big banks are bad.”

It’s about which system actually makes sense today.

Why I Ultimately Chose Wealthsimple

What sold me wasn’t just the lack of fees—it was how frictionless everything felt.

I can:

- Open accounts quickly

- Move money freely

- Invest, save, buy crypto, and file taxes in one place

- Get support without wasting time

And most importantly, I’m no longer paying $192 a year just for the privilege of existing financially.

Want to Try It?

If you’re curious and want to check it out, here’s my invite link:

👉 https://www.wealthsimple.com/invite/DKM6MQ

No pressure—just sharing what genuinely worked better for me.

Final Thought

Paying a monthly fee for a chequing account used to feel “normal.”

Paying extra just to file taxes on top of that? Even worse.

Once I questioned all of it, switching to Wealthsimple became an easy decision—and one I wish I’d made sooner.

Discover more from ByteFlip

Subscribe to get the latest posts sent to your email.